Discovering the diamond in the rough, the overlooked gem, is a feeling akin to striking gold before the masses catch on. Tom and David Gardner’s early support of Amazon.com and Netflix (NASDAQ: NFLX) laid the foundation for the success of The Motley Fool. Reflecting on my personal journey, I delved deep into the realms of the internet back in 1995, navigating the nascent world wide web at a snail’s pace from a Swedish college computer room, an adventure that eventually led me to Florida through an online game encounter.

Fast forward to today, still hitched to the American sweetheart I met online almost three decades ago, my entire professional life hinges on the digital realm. The internet, indeed, has been a game-changer for me.

While I make no claims to clairvoyance, I possess the foresight honed by heeding the Gardner brothers’ wisdom long before penning my words at The Motley Fool. And much like my early embrace of the internet era, I’ve unearthed two companies displaying the markers of extraordinary long-term growth, reminiscent of Amazon and Netflix in their infancy.

Roku: The Purposeful Plunge Upholding Strategy

In a curious twist of fate, the first contender on my list, Roku (NASDAQ: ROKU), once operated under Netflix’s umbrella. Initially crafting devices for streaming Netflix content from laptops to TVs, Roku weathered the storm of DVD-mailer bloom to digital streaming bust. Investors alert enough to grab Netflix shares during the Qwikster debacle reaped substantial returns over time, a move mirrored by my own investment from October 2011 yielding a jaw-dropping 5,000% surge.

Parallel to Netflix’s narrative in bygone years, Roku’s current slump in stock value presents an opportunity shrouded in unfounded apprehensions. Pessimists dote on surface-level metrics; Roku’s revenue growth decelerated in 2022–2023, tipping earnings into the red. Yet, history echoes anew – these transient fiscal dips are strategic maneuvers enacted amidst an inflationary downturn.

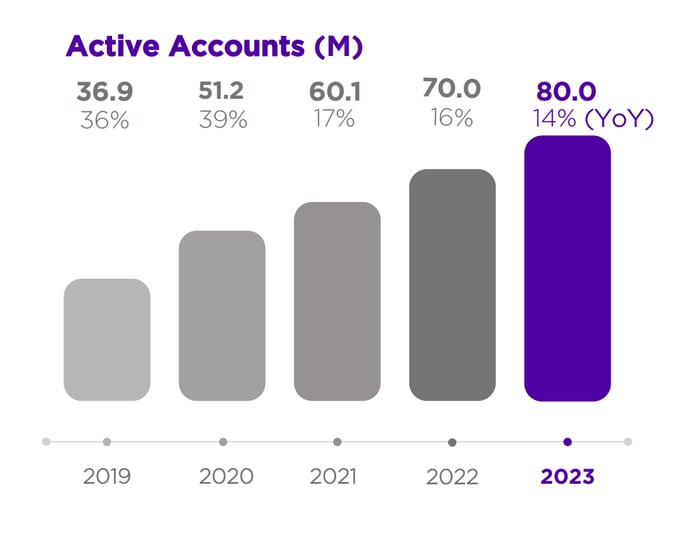

While many players hiked prices to offset growing costs, Roku played a distinct hand, maintaining pricing stability to lure in more consumers and expand its market dominion during economic turbulence. The gambit paid off handsomely, evidenced by a surge in Roku accounts from 70 million to 80 million within a year.

Chart source: Roku’s Q4 2023 earnings report.

Despite its negative earnings tag, Roku’s cash profits pulse healthily upwards. Converting 5% of its 2023 revenues into free cash flows, Roku flaunts buoyant cash inflows fueled by stock-based compensation and video content amortization. The emphasis on cash flows underscores tangible monetary movements, distinct from earnings as an accounting tool. Viewing low or negative earnings alongside robust cash flows as fiscal finesse to mitigate tax burdens is prudent, not peeking potholes but laying gravel for smoother taxes.

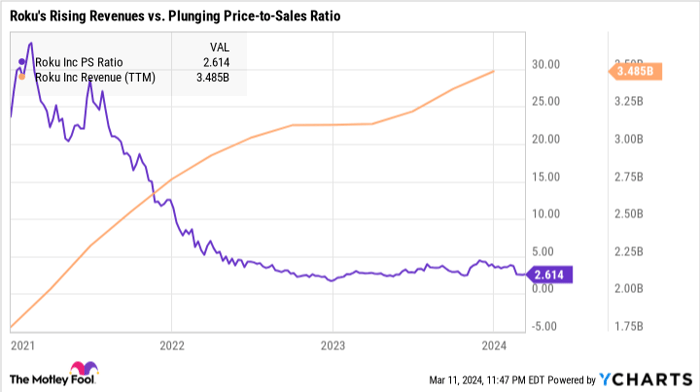

While the media and entertainment ad sector languishes in the shadow of the inflationary tempest, hobbling Roku – a substantial revenue contributor perched on M&E ads bulwark – this caliginous phase shall ebb. The market’s myopic fixation on Roku’s M&E obstacles and bottom-line blues has dredged stock prices to sink over 85% beneath peak values of yesteryears. A beeline for Roku shares now nets a meager 2.7 times sales valuation, a steal squarely positioning Roku as a staid revenue mill rather than an emerging contender ripe for exponential growth. Patience, dear investors, lest you dash at discount’s end for Roku’s justified ascension:

ROKU PS Ratio data by YCharts

AI Magic: Voices of Tomorrow with SoundHound AI

Transitioning to our next prospect, SoundHound AI (NASDAQ: SOUN) breaks through as a provider of voice control and audio analytic solutions, catering to automotive, drive-through locales, phone-menu establishments, and beyond. Noteworthy is SoundHound AI’s orchestrating role in Netflix’s set-top box reference design voice features since 2019.

Leveraging cutting-edge artificial intelligence (AI) engines, entrenched in years of song recognition services and contextualized by ongoing voice-command influx, SoundHound AI surpasses rudimentary speech-to-text norms with its deep learning ecosystem, heralding a superior user experience.

The Resilient Growth of SoundHound AI and the Potential in A Crowded Market

Subtle Presence, Substantial Impact

SoundHound AI may be on the quieter side when it comes to branding, often masked by client choices to foreground their own identities instead. From powering voice control systems in Stellantis vehicles to enhancing the drive-through experience at White Castle, the omnipresence of SoundHound’s Houndify platform is stealthy yet profound.

A Meteoric Rise Amidst Financial Modesty

Despite its unassuming profile, SoundHound AI is a force to be reckoned with in the world of AI technology. With revenues hitting $46 million in fiscal year 2023 and a backlog of orders and contracts totaling a staggering $661 million, the company is setting the stage for substantial growth. The doubling of its backlog within a year underscores the exponential trajectory it is on.

Investment Potential and Market Dynamics

Recent alignment with industry behemoth Nvidia and a dip in stock price relative to its IPO valuation in 2021 hint at potential undervaluation. While the price-to-sales ratio may induce sticker shock, the robust bookings backlog provides a solid foundation for future growth. The historical trend of niche specialists in voice control and audio analysis being prime acquisition targets bodes well for SoundHound AI in a competitive market.

A Glimpse Into the Future

Comparisons with industry giants like Netflix and Amazon signal the growth potential of SoundHound AI and Roku, despite their current undervaluation. Drawing parallels to the disruptive journeys of these tech stalwarts offers a compelling narrative for investors seeking promising growth stocks. The tantalizing prospect of another bidding war for a voice-control virtuoso in the making adds to the allure of SoundHound AI.

Invest Wisely

While speculation abounds about the future of SoundHound AI, weighing options and consulting expert advice is prudent. Potential investors are urged to tread carefully and consider the comprehensive analyses provided by investment services like the Motley Fool. A historical perspective on market performance and expert recommendations can be invaluable tools in navigating the unpredictable waters of the stock market.

Disclosure and Final Thoughts

It’s worth noting the industry affiliations of prominent figures like John Mackey and Anders Bylund, shedding light on their investments in tech giants and their perspectives on emerging players like SoundHound AI. While the path to growth may be riddled with uncertainties and risks, the allure of a resilient underdog making waves in a competitive market is undeniably captivating.