The pulsating beats of the stock market barely flinched after July’s subdued inflation reveal on Wednesday. The Nasdaq seemed entangled beneath its 21-day moving average, an impending wall of resistance post its swift ascent from the tech-heavy index’s 200-day nadir.

Speculations are rife among Wall Street traders, predicting a turbulent road ahead over the next few months leading into the presidential elections. The market braces for potential near-term convulsions amidst amplified volatility, especially as many tech equities boast considerable gains, soaring over 20% year-to-date.

Image Source: Zacks Investment Research

Fortunately, the dual titans of the market—interest rates and earnings—persist as bullish gusts propelling the markets forward, poised to swoop in and staunch any substantial market retreats.

Today beckons exploration into two esteemed large-cap tech entities—Micron (MU) and Advanced Micro Devices (AMD)—both languishing at least 30% off their peaks, offering investors a prospect of long-term growth within the domain of artificial intelligence and beyond.

Delving into Micron’s Prospects During a 33% Dip from Highs

Unveiling the essence: Micron (MU) emerges as a semiconductor behemoth reveling in the AI upsurge, poised to witness sales surge by over 50% in FY24 and FY25, positioned 33% beneath its zeniths.

Micron commands the realm of memory chips, flaunting an expanding repertoire of DRAM and NAND offerings. Riding the wave of the booming PC, smartphone, and data center landscapes, Micron professed its enthralling journey through the annals of artificial intelligence. Behold, MU now embarks on its AI odyssey.

MU unleashes chips meticulously crafted to uphold the burdensome tasks demanded by AI data domains. Vigorously broadening its manufacturing horizon, Micron showers billions into capex to erect state-of-the-art memory fabs across the U.S.

Image Source: Zacks Investment Research

Micron anticipates an unprecedented demand for memory chips catalyzed by the AI skirmish. Witness the splendor as MU escalates its Q3 FY24 sales (disclosed in late June) by a resounding 82%. AI yearnings fuel a 50% sequential data center revenue surge, crowned by an all-time high data center revenue mix. Expected is a record revenue haul in FY25, propelled by an insatiable “robust AI demand.”

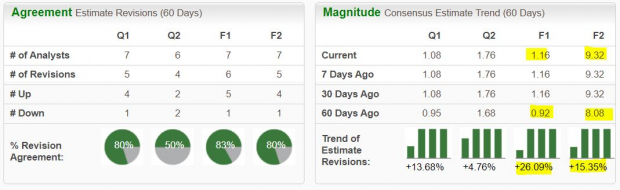

Projections envision a 60% revenue leap in FY24 and another 55% in FY25 for MU, culminating in a lofty $38.63 billion—shattering FY22’s $30.76 billion pinnacle. On the profit frontier, Micron shall somersault from an adjusted loss of -$4.45 per share last year to $1.16 in FY24, and skyrocket by a staggering 700% in FY25, arriving at $9.32 per share.

Micron’s FY24 consensus earnings outlook vaulted 26% since its Q3 unveil, with FY25’s consensus marking a 15% uptick. Micron’s sanguine EPS vista earns it a coveted Zacks Rank #2 (Buy). Fortified by a robust balance sheet, Micron fortifies its growth undertakings in tandem with rewarding dividend disbursements.

Image Source: Zacks Investment Research

Over a decade and a half, Micron shares outpaced the Zacks Tech sector. A commendable 42% ascent in the trailing three months positions MU ahead of Tech’s 20%, inclusive of Micron’s 33% descent from its zeniths in June. Trading at a discount of 55% to the Zacks Tech sector and over 60% under various past peaks in the last decade, Micron trades at 11.6X forward 12-month earnings, exuding tremendous potential.

Seizing the Opportunity with Advanced Micro Devices (AMD) for Long-Term Growth

Unveiling the essence: Advanced Micro Devices (AMD) steers its course to capture a share of the AI chip domain from its GPU adversary and industry juggernaut Nvidia (NVDA). AMD, slated to upscale its adjusted earnings by 26% this year and a luminous 54% the next, finds itself plummeting over 30% from its peak in March.

A standout luminary in the realms of GPU and CPU, AMD’s cardinal GPU sector burgeoned alongside the gaming domain, data centers, and beyond over the bygone decade. Witness AMD’s astounding ascent, cranking its revenue from a modest $4 billion in FY15 to a near $23 billion crescendo last year.

AMD finds itself trailing behind AI chip sovereign Nvidia. Yet, amid the colossal AI realm, AMD savors abundant spoils akin to Nvidia. AMD’s strategic acquisition of Silo AI—the European AI citadel—on August 12 in a $665 million all-cash pact aims to “expedite AI model development and deployment on AMD hardware.”

Image Source: Zacks Investment Research

AMD triumphed over our Q2 EPS estimations on July 30, albeit slightly subdued in guidance projection, prolonging its streak

Analyzing AMD’s Growth Trajectory Amidst Industry Challenges

Despite facing downward revisions in its revenue forecasts, Advanced Micro Devices (AMD) is projected to demonstrate impressive growth figures in the coming years. AMD is expected to achieve a 13% revenue increase in 2024, followed by a significant 26% rise in sales the next year, projected to reach $32.18 billion by FY25. Moreover, the company aims to elevate its adjusted earnings by 26% this year and a remarkable 52% in the subsequent year.

AMD’s strategic focus on Artificial Intelligence (AI) reflects a long-term growth strategy. CEO Dr. Lisa Su highlighted the company’s commitment to capitalize on the burgeoning demand for compute power in AI applications, envisioning substantial growth opportunities as AMD continues to offer cutting-edge AI solutions across its business segments.

Financial Performance and Market Position

Over the past decade, AMD’s shares have outshone the broader Tech sector by a staggering 3,300%, surpassing the Zacks Semiconductor market by a substantial margin of 920%. However, recent market trends have seen AMD underperforming compared to the chip industry, with a 5% decline year-to-date and a 33% drop from its early 2021 records.

In an effort to stabilize its position, AMD is seeking support around its 21-month moving average. The stock is currently trading at historically oversold RSI levels witnessed over a decade, oscillating between its 21-week and 50-week moving averages. Additionally, investors are actively trying to prevent AMD’s stock from slipping significantly below its 2021 peak levels.

Valuation and Market Comparisons

Compared to its five-year highs, AMD is trading at a 45% discount with a forward 12-month earnings multiple of 38.5X, bringing it in line with the Zacks Semiconductor Market average. Furthermore, its Price/Earnings to Growth (PEG) ratio, which considers long-term earnings potential, offers a conservative outlook compared to the broader Tech sector and reflects an 82% discount from AMD’s recent valuation peaks.

Despite being the secondary player in the AI chip market, often likened to Pepsi compared to Nvidia’s Coca-Cola, AMD has carved a significant niche for itself as a strong contender in this realm. Securing the second spot stands as a remarkable achievement, showcasing the company’s solid positioning within the competitive landscape.