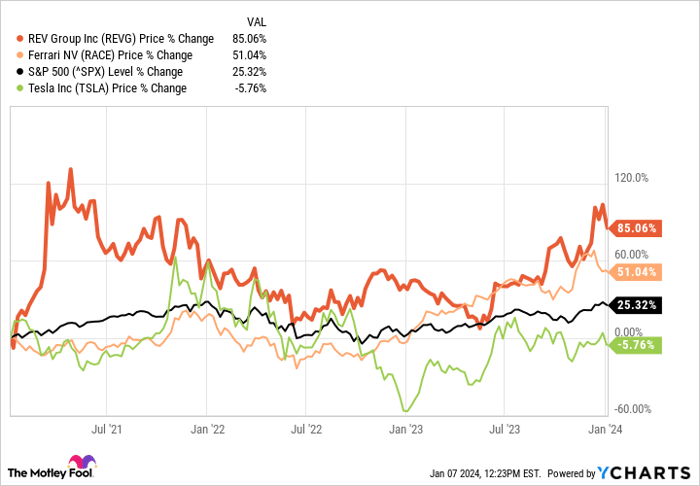

There exists a stock in the automotive industry so obscure, it has managed to outshine Tesla and Ferrari, surpassing the S&P 500 by threefold in the past three years. In the world of dividends, it’s a diamond in the rough. Breathe in REV Group, dear investors – a name you’ve hardly encountered. Yet, this is an opportunity you cannot afford to overlook. Here’s why.

The Path Less Traveled: REV Group 101

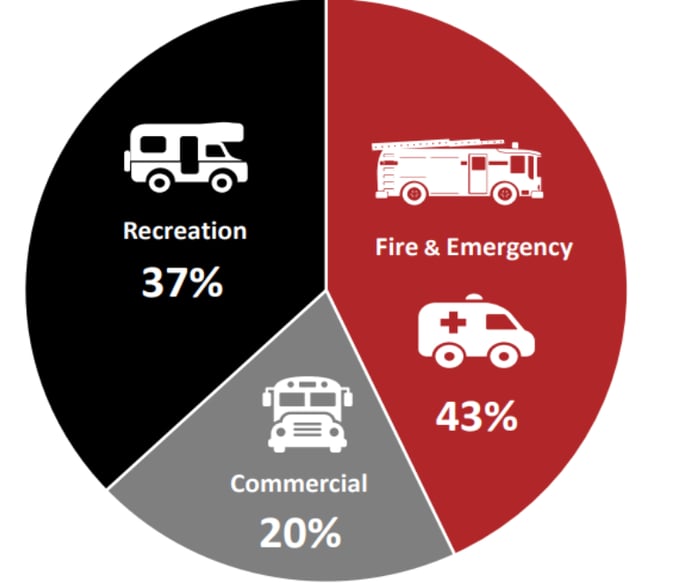

REV Group dominates as a premier designer and producer of specialty vehicles and complementary aftermarket parts and services. Its operations excel across three key sectors: fire & emergency, commercial, and recreation.

REV Group (REVG) TTM sales through Q3; TTM = trailing 12 months. Image source: REV Group.

Consider the myriad public service agencies purchasing ambulances, fire trucks, school buses, transit buses, industrial sweepers, and even recreational vehicles – they overwhelmingly turn to REV Group for these requisites.

Now let’s delve into the strength of its ongoing enterprise, the flourishing backlog of orders, and a singular catalyst that could propel the company’s stock to even greater heights.

A Profusion of Orders

For investors, nothing quite instills confidence like a thriving backlog of orders. This type of revenue transparency is reassuring, and REV Group’s backlog is undeniably impressive at a staggering $4.5 billion.

To add context to this figure, the backlog nearly equals two years’ worth of net sales – the company’s estimated full-year 2024 net sales hover between $2.6 billion and $2.7 billion.

Next, let’s closely examine the segment propelling this backlog of orders.

Heat & Haste: Fire & Emergency

REV Group’s paramount category currently lies in fire & emergency. With a record backlog of $3.6 billion at year-end 2023, not only is it steering the company’s progress, but it also stands poised to drive future profits.

What’s even better for investors: heightened profitability. Net sales surged from $253 million in the fourth quarter of 2022 to $339.1 million a year later. A truly striking leap emerges in the segment’s adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA), surging from $1.9 million to $26.8 million over the same period.

The surge in profitability arose from manpower retention efficiency gains, heightened commencements and completions (essentially, streamlining operations and throughput), and the adeptness to enforce price hikes.

Investors ought to recognize that REV Group’s fire & emergency segment is vulnerable to seasonal fluctuations, with management anticipating a customary deceleration during the first quarter of 2024 due to fewer working days.

A Leap in Leisure: The Recreation Catalyst

The commercial segment of REV Group has maintained steadiness while experiencing growth. Furthermore, it has displayed a robust backlog for school buses, offset by subdued demand for terminal trucks and street sweepers. The adjusted EBITDA margin for the category soared from 3% in the fourth quarter to…

The REV Group Struggles Amidst Declining Demand in the Recreation Market

The REV Group has faced a tough year, with their stock plummeting from a 52-week high of 45.16% in Q2 of 2022 to nearly 12% a year later. Though the company exhibited surging margins in two of its three segments, the real catalyst was the decline in the recreation category, due to soft demand for towables and camper units. This resulted in a 66% decrease in their 2023 year-end backlog, offsetting price increases with discounting in slow-growth categories.

The Impact of Low Recreation Demand

Management has been focused on implementing cost-saving measures and retaining labor to counter the demand weakness. However, they are hopeful for a boost in recreational demand heading into spring and summer, which could significantly contribute to the segment’s and the company’s overall bottom lines.

Investor Considerations

The stock’s future remains uncertain. While it may be a tall task to expect the REV Group to triple the market performance again over the next three years, it’s important to note that the company not only sells finely-tuned machines but is also becoming a finely-tuned machine itself, evident from its surging margins in two of its three segments.

Another positive aspect for investors is the fact that the company trades at a fair price-to-earnings ratio of 22 times, coupled with a 1.2% dividend yield that could potentially grow with improved margins and a rebound in recreational vehicle sales. However, with REV Group not making the cut for the ’10 best stocks’ to buy now, as identified by the Motley Fool Stock Advisor analyst team, investor caution is advisable.

If the company doesn’t seem like a buy for investors at present, it might be wise to keep an eye on REV Group for any potential dips that could provide an opportune moment to scoop up shares.

Ultimately, with a downturn in the recreation category and increased competition from other market segments, investors should weigh this cautiously before making any investment decisions.

*Stock Advisor returns as of December 18, 2023

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.