Adobe ADBE shares dropped 5.8% post the first-quarter fiscal 2026 results reported on Thursday (March 12), last week. The drop can be attributed to the departure announcement of long-term CEO Shantanu Narayan, a modest 10.9% growth in annualized recurring revenues (ARR) and intensifying competition. The CEO transition adds to the investor risk in a challenging environment as Adobe continues to play a catch-up role in the AI domain against the likes of Microsoft MSFT, OpenAI, Alphabet GOOGL, Salesforce CRM, Midjourney and Canva.

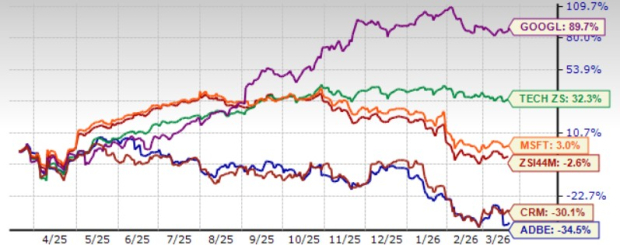

ADBE shares have plunged 34.5% in the trailing 12-month period, underperforming the Zacks Computer and Technology sector’s appreciation of 32.3% and the Zacks Computer – Software industry’s decline of 2.6%. Shares of Alphabet and Microsoft have returned 89.7% and 3%, respectively, while Salesforce has plunged 30.1% over the same time frame. So, how should investors approach the Adobe stock right now? Let us find out.

ADBE Stock’s Performance

Image Source: Zacks Investment Research

Adobe Reports Strong Q1 Results, ARR Outlook Disappoints

Adobe’s earnings of $6.06 per share beat the Zacks Consensus Estimate by 3.06% while revenues of $6.398 billion surpassed the consensus mark by 1.86%. Earnings increased 19.3% year over year on 12% reported growth in revenues.

ARR hit $26.06 billion in the reported quarter, and growth (10.9%) reflected the negative impact of rising monthly active users (MAUs) of new products. AI-first offerings (Acrobat Studio with Adobe Express, Firefly and GenStudio) ending ARR more than tripled year over year in the reported quarter. Creative freemium MAU crossed 80 million, growing 50% year-over-year and includes web and mobile versions of Firefly, Express, Premiere, Photoshop and Lightroom in the reported quarter. Adobe still targets ARR growth of 10.2% for fiscal 2026, driven by an innovative AI-powered portfolio, the expanding adoption of enterprises and a large market opportunity.

For the second quarter of fiscal 2026, Adobe expects total revenues between $6.43 billion and $6.48 billion. The Zacks Consensus Estimate for revenues is currently pegged at $6.46 billion, indicating 9.9% growth from the figure reported in the year-ago quarter.

Adobe expects fiscal second-quarter non-GAAP earnings between $5.85 and $5.90 per share. The consensus estimate for earnings is currently pegged at $5.70 per share, up 3 cents over the past 30 days, indicating 12.7% growth from the figure reported in the year-ago quarter.

Adobe Inc. Price and Consensus

Adobe Inc. price-consensus-chart | Adobe Inc. Quote

Can Adobe’s Growing AI Push Steer Off Competition?

Adobe’s prospects in fiscal 2026 and beyond will depend much on the success of its ongoing and future AI initiatives. Ongoing AI push is helping in advancing the company’s footprint among business, creative and marketing professionals. In the first quarter of fiscal 2026, Adobe surpassed 850 million monthly active users of Acrobat, Creative Cloud, Express and Firefly, achieving 17% year-over-year growth. ADBE achieved more than 30% year-over-year growth in Adobe Experience Platform and apps, as well as Adobe GenStudio, ending ARR.

Adobe’s business professionals and consumer business are benefiting from solutions like PDF Spaces and Acrobat AI Assistant. Acrobat and Express integrations are empowering users to turn content they are consuming into generated presentations, infographics, audio summaries and more. AI Assistant MAU doubled year-over-year and Express MAU tripled year-over-year in the first quarter of fiscal 2026. Express is currently used in 99% of U.S. Fortune 500 companies.

Adobe is benefiting from an expanding partner base and integrations with leading AI ecosystems, including Amazon Web Services, Azure, Google Gemini, Microsoft CoPilot and OpenAI. In the first quarter of fiscal 2026, Adobe launched Acrobat and Express for ChatGPT and expects to see similar integrations into Copilot, Claude and Gemini. Enterprise collaborations with the likes of Accenture, Cognizant, Deloitte, Dentsu, EY, IBM, Infosys, Omnicom, Publicis, PwC, Stagwell, TCS and WPP bode well for the company’s prospects.

Nevertheless, stiff competition is a headwind. Adobe’s AI-related revenues are minuscule compared with Microsoft, Alphabet and Salesforce. Microsoft’s Intelligent Cloud revenues are benefiting from growth in Azure AI services and a rise in the AI Copilot business. Alphabet’s focus on infusing AI heavily across its offerings, including Search and Google Cloud, has been a major growth driver. Salesforce’s strategy of continuous expansion of generative AI offerings is helping it tap growth opportunities.

Here’s Why Adobe Shares are a Hold Now

Adobe has a Value Score of B, which suggests a cheap valuation. In terms of price/earnings (P/E), Adobe shares are trading at 10.44X lower than the broader sector’s 24.06X.

ADBE’s Valuation

Image Source: Zacks Investment Research

Adobe’s continuing AI integration into its solutions, an innovative portfolio and rich partner base are positives for investors already holding the stock. However, AI-related disruption, softer ARR growth, headwinds related to the CEO transition, and stiff competition make the stock a risky bet in the near term for prospective investors.

ADBE currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the “first wave” of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks’ AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Salesforce, Inc. (CRM) : Free Stock Analysis Report

Adobe Inc. (ADBE) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.