Intel Corporation INTC has taken a nosedive of 55.8% year to date, a stark contrast to the industry’s robust growth of 97.8%. In a race where Intel’s competitors like Advanced Micro Devices, Inc. and NVIDIA Corporation are sprinting ahead, Intel finds itself stumbling, grappling with financial turmoil and operational hurdles that have prompted a deep introspection of its core.

The company is soul-searching, contemplating potential solutions such as splitting its product design and manufacturing divisions, canceling certain factory projects, and setting up Intel Foundry as an independent entity. This strategic reevaluation aims to streamline operations, enhance efficiency, and detach the Foundry, which reported an operating loss of $2.8 billion in the previous quarter, from the rest of Intel.

YTD Price Performance

Image Source: Zacks Investment Research

Challenges Haunt INTC’s Margins

Intel is expanding its presence in artificial intelligence, with initiatives in edge devices and PCs powered by Core Ultra processors supporting numerous software vendors and AI models. The Lunar Lake architecture, boasting advanced AI processing abilities, offers substantial performance and energy efficiency gains. Moreover, Intel’s unveiling of next-gen products like the Intel Xeon 6 processors and the Intel Core Ultra client processors cements its leadership in the AI domain.

Despite its bold moves in the AI space, Intel’s margins are suffering from the aggressive rollout of AI PCs, particularly as production has shifted to a higher-cost facility in Ireland. Other margin-denting factors include charges related to non-core businesses, unused capacity, and an unfavorable product mix. Intense pricing pressures from competitors are adding to its profitability woes.

Image Source: Zacks Investment Research

INTC’s Woes in Soft China Market and Trade Turmoil

With China accounting for over a quarter of its revenues, Intel is facing headwinds from the country’s push to swap out U.S.-made chips with domestic alternatives. Beijing’s ambition to minimize reliance on Western tech and recent directives to eliminate foreign chips from vital networks by 2027 are squeezing Intel’s revenue stream. Tightening restrictions on high-tech exports to China are intensifying local chipmakers’ competition, posing a dual threat to Intel’s market share.

Furthermore, sluggish spending in consumer and enterprise sectors in China has led to elevated customer inventories, with management anticipating a reduction in inventory levels over the remainder of the year. Export controls and market dynamics are likely to restrain revenue growth, with flat to declining business in the client segment and moderate growth in data center and edge markets.

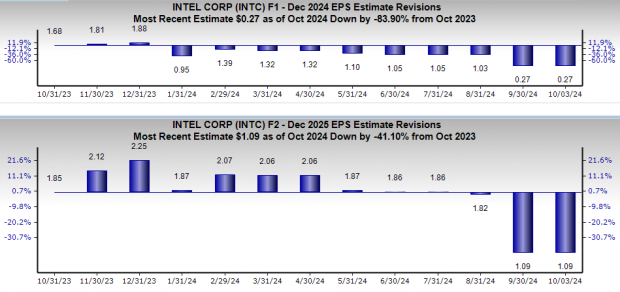

Revision Trend for INTC’s Estimates

Earnings projections for 2024 have plummeted by 83.9% to 27 cents over the last year for Intel, while estimates for 2025 have dipped by 41.1% to $1.09. Such downward revisions signal bearish sentiment surrounding the company’s stock.

Image Source: Zacks Investment Research

Parting Thoughts

Intel’s strides in AI solutions hold promise for the semiconductor industry, breaking new ground in scalability, performance, and interoperability. Despite these advancements, being rated a Zacks Rank #4 (Sell), the timing of its recent product launches may be too little, too late. Mounting margin challenges, aggravated by export decrees, an unfavorable product mix, and bloated customer inventories, cast a shadow on its profitability. With diminishing earnings estimates and lackluster stock performance compared to peers, investor sentiments are turning sour. Consequently, putting faith in the stock at this juncture may be a gamble best avoided.

Market News and Data brought to you by Benzinga APIs

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.