Amazon (NASDAQ: AMZN) experienced an astounding surge of approximately 75% in 2023, eclipsing the total returns of the S&P 500 index threefold. The e-commerce and cloud-computing giant made a momentous turnaround from a challenging 2022, resulting in rejuvenated investor confidence. With a market capitalization exceeding $1.5 trillion, Amazon now ranks as the fifth-most valuable company globally.

While the stock’s substantial gains may lead some to believe they’ve missed the boat, such exponential growth doesn’t necessarily signal a missed opportunity. Is Amazon poised to outperform the market once more in 2024? Let’s delve into the factors at play.

A Traversal of Margin Dynamics in E-Commerce

Amazon’s operational breadth encompasses diversified interests, yet the fulcrum of its operations revolves around e-commerce and cloud computing. For years, skepticism shrouded Amazon’s e-commerce segment, with concerns about its ability to yield profitability, primarily in the United States due to the extensive geographic dispersal of the population.

However, in late 2023, Amazon laid these lingering doubts to rest. Bolstered by its expansive logistics infrastructure, burgeoning advertising revenue, and a surge in high-margin third-party seller fees, the e-commerce segment displayed signs of burgeoning margins, particularly in North America. The last quarter evidenced a 4.9% operating margin in Amazon’s North American segment, marking a substantial ascent from a negative 0.5% a year earlier.

The ongoing margin expansion in the North American segment, driven by the ongoing capacity build-out post-COVID-19, robust growth in advertising, and third-party sales, suggests a potential attainment of 10% operating margins in 2024. Such a feat would translate to $34 billion in earnings, underpinning the momentum of online shopping as it continues to gain market share, galvanized by a relatively low 20% penetration of overall retail sales. This indomitable industry tailwind is anticipated to propel Amazon’s revenue to loftier heights in the foreseeable future.

The Underestimated Ascendancy of Cloud Computing

Amazon’s most lucrative segment, Amazon Web Services (AWS), its cloud computing division, is nearing $100 billion of revenue, boasting operating margins exceeding 25%. Notably, the cloud computing. division conveys a resilience grossing a 12% increase in revenue year-over-year last quarter, defying apprehensions of decelerating growth as a result of its entrenchment in the computing infrastructure of numerous companies.

Meanwhile, AWS remains poised for continued growth buoyed by the surge in cloud computing demand, the flourishing artificial intelligence domain, and the escalating global computing requisites. Should AWS hit the $200 billion revenue milestone within the next five to six years while maintaining its market share, it could translate to a formidable $50 billion in operating income for Amazon, further cementing its prowess as a profit-generating engine.

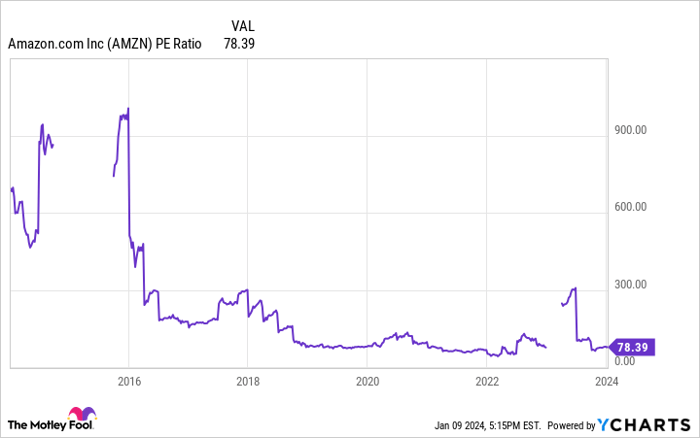

AMZN PE Ratio data by YCharts. PE Ratio = price-to-earnings ratio.

But is the stock cheap?

Despite an apparent trailing price-to-earnings (P/E) ratio of 78, Amazon’s current market capitalization of $1.56 trillion belies a stock seemingly overpriced at first glance. However, a myopic focus on the trailing P/E fails to foreground the rapid margin expansion in e-commerce and the immense growth prospects inherent in the cloud computing segment.

If Amazon’s North American retail division attains the projected 10% margins and $34 billion in earnings, coupled with the anticipated $25 billion earnings from cloud computing, the combined earnings of $59 billion offer a recalibrated perspective. Currently undervalued, this valuation doesn’t even account for the international retail operations and experimental ventures such as Kuiper satellite internet or healthcare. This analytical reframe yields a comparative P/E ratio of 26, akin to the market average and significantly more digestible than the apparent P/E of 78.

The undervalued status of Amazon’s stock, coupled with ample room for top-line growth, bodes well for the company’s prospects, portending its potential to once again surpass market expectations in 2024. A technology luminary of this caliber certainly warrants close attention.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for two decades, Motley Fool Stock Advisor, has more than tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Amazon made the list — but there are 9 other stocks you may be overlooking.

*Stock Advisor returns as of January 8, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Brett Schafer has positions in Amazon. The Motley Fool has positions in and recommends Amazon. The Motley Fool has a disclosure policy.