In the fierce competition for dominance in the realm of semiconductors, the battleground is currently occupied by two titans – Nvidia (NASDAQ: NVDA) and Advanced Micro Devices (NASDAQ: AMD). Over the last five years, both entities have demonstrated significant market performance. Remarkably, AMD’s stock has surged by a remarkable 433% during this period. However, this substantial growth is eclipsed by Nvidia’s astronomical stock surge of over 3,000%.

While Nvidia has held the crown as the superior performer in the last five years, an intriguing question looms – which company is poised to outshine the other in the next five?

The Battle: Nvidia vs. AMD

At present, the expansion of artificial intelligence (AI) infrastructure favors both companies owing to the heightened demand for graphic processing units (GPUs) essential in powering large language model (LLM) training and artificial intelligence (AI) inference. This escalating need for GPUs drove Nvidia’s data center segment to achieve a staggering $22.6 billion in fiscal 2025 Q1 revenue, marking a phenomenal 427% year-over-year surge. In contrast, AMD’s data center segment witnessed a more than 80% increase year over year, reaching $2.3 billion in fiscal 2024 first-quarter revenue.

Nvidia has distinctly emerged as the frontrunner in the AI chip domain. Evident in its data center segment generating nearly ten times the revenue produced by AMD’s data center segment. Nvidia’s GPUs reign supreme, primarily due to its CUDA (Compute Unified Device Architecture) software platform, which developers have extensively trained on for chip programming. Consequently, this has fortified a substantial moat for Nvidia’s GPUs, securing over 80% market share.

Nevertheless, AMD is making significant strides. Recently, Microsoft (NASDAQ: MSFT) unveiled plans to offer clusters of AMD’s MI300X chips through its Azure cloud computing service as an alternative to Nvidia. Furthermore, AMD disclosed serious inquiries regarding constructing an AI cluster with over 1 million GPUs – a potential game-changer. Traditionally, enterprises prefer multiple suppliers to avert reliance on a single entity.

While Nvidia’s narrative predominantly revolves around its GPU products and data center segment, constituting 87% of its revenue, AMD’s data center segment accounts for just 43% of its total revenue. Simultaneously, certain other segments of AMD grapple with challenges, resulting in a mere 2% year-over-year revenue growth in the quarter compared to Nvidia’s impressive 262% surge.

Image source: Getty Images.

Optimal Investment Choice: Evaluating the Stocks

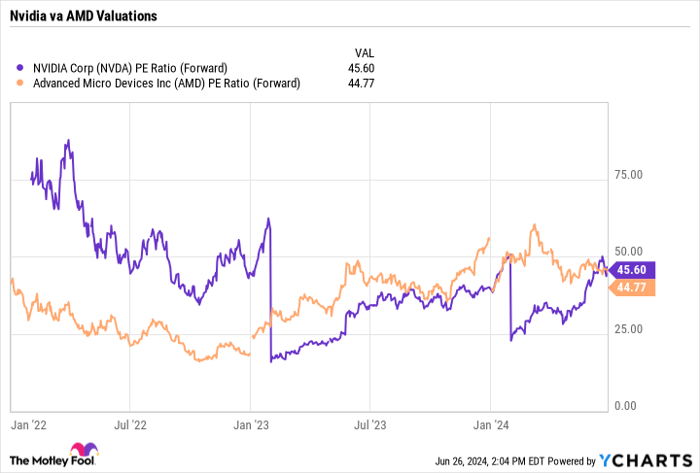

Despite Nvidia’s robust stock performance, both stocks currently sport almost identical forward price-to-earnings (P/E) valuations. Nvidia boasts a 45.6 forward P/E ratio, slightly higher than AMD’s 44.8.

NVDA PE Ratio (Forward) data by YCharts.

Given the closely matched valuations, the superior stock selection in terms of operational performance over the next few years becomes pivotal.

AMD enjoys the advantage of its data center segment possessing a smaller foundational base compared to Nvidia. As the underdog, AMD stands a chance to erode Nvidia’s market share. A successful metamorphosis into a reliable secondary source of GPU chips could spell prolonged growth in the segment.

Looking towards the distant horizon, AMD’s gaming segment – which has previously lagged – is anticipated to witness a monumental upswing by 2027 or 2028. Reports indicate Microsoft’s imminent launch of its next-gen gaming console in 2028, while Sony anticipates unveiling its PlayStation 6 console in 2027 or 2028.

In 2022, revenue stemming from the Sony PlayStation 5 (PS5) at AMD stood at an impressive $3.8 billion, constituting 16% of its revenue. Typically, console sales peak in the third year post-launch, and the PS5 was introduced in 2020.

Conversely, Nvidia’s forte lies in the formidable moat fashioned by its CUDA platform. Developers have acclimated to its platform, rendering familiarity with other GPUs time-consuming and cost-intensive. This positions Nvidia to retain its lead.

Concurrently, AMD aggressively embarks on innovation with the development of next-gen architecture GPU platforms compatible with its existing architecture. This forward-thinking approach is poised to drive substantial demand from customers seeking cutting-edge AI capabilities.

If AI is still in its nascent stages and the data center expansion is in its embryonic phase, Nvidia emerges as the prime choice between the two chip giants, owing to the robust moat it has erected. Nonetheless, AMD presents a compelling investment prospect, especially with an impending gaming console refresh cycle in the coming years.

Contemplating the $1,000 Investment in Nvidia

Prior to venturing into investing in Nvidia stock, contemplate this:

The Untapped Potential: Unveiling the True Titans of Investment

10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $757,001!

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 24, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.