The semiconductor sector has surged on the market, as exemplified by the 61% jump in the PHLX Semiconductor Sector index. Two constituents of the index, Nvidia and Advanced Micro Devices (AMD), have also reaped the benefits. Nvidia’s shares have skyrocketed by a whopping 252% over the past year, while AMD’s have seen a robust 128% increase. Both companies are expected to continue their hot streak through 2024, capitalizing on the anticipated growth of the semiconductor industry.

According to Gartner, global semiconductor revenue is estimated to rise by 17% in 2024 to $624 billion. This substantial improvement comes after a decline of 11% in the previous year, owing to weaknesses in the smartphone and PC markets, along with restrained spending in the enterprise data center sector.

Nvidia’s Prospects

Amidst the semiconductor downturn last year, the demand for chips used in artificial intelligence (AI) servers for training large language models (LLMs) remained strong. Nvidia capitalizes on this trend and is projected to conclude the ongoing fiscal year 2024 with $59 billion in revenue, a significant leap from the $27 billion generated in the previous fiscal year.

Nvidia’s future looks promising as the demand for AI chips is expected to continue its rapid growth. Investment bank UBS forecasts the AI graphics cards and chips market to grow at an annual rate of 60% through 2027, generating annual revenue of $165 billion. Moreover, Nvidia is expected to maintain a dominant 85% share of this flourishing AI chip market in 2024, which should drive substantial growth in the company’s data center revenue.

Analyst Srini Pajjuri predicts that Nvidia’s data center business could achieve $65 billion in revenue in fiscal 2025, representing a 66% increase. Furthermore, the demand for the company’s graphics cards used in gaming PCs is anticipated to rise, thanks to a market turnaround and the adoption of AI-enabled computers.

These factors point to a significant jump in Nvidia’s total revenue by 56% in fiscal 2025 to $92 billion. Additionally, its earnings are projected to increase by 66% in the upcoming fiscal year to $20.44 per share, making it an appealing choice for growth-oriented investors.

AMD’s Position

Unlike Nvidia, which derives 80% of its total revenue from selling data center chips, the majority of AMD’s revenue comes from selling CPUs, graphics cards, and semi-custom chips used in PCs and gaming consoles. This year, the recovery in the PC market is expected to be a crucial driver for AMD, with Canalys forecasting an 8% increase in PC shipments. This represents a positive turnaround following a 12% decline last year.

AMD has positioned itself to capitalize on the market for AI-enabled PCs with its CPUs, which is expected to unlock long-term growth potential as AI-powered PCs are projected to achieve annual growth of 50% through 2030. Despite these opportunities, the company’s gaming segment could continue to hinder its performance, with revenue from this segment down 8% in the third quarter of 2023 due to tepid sales of its semi-custom chips used by Microsoft and Sony in their gaming consoles.

AMD’s growth is expected to be slower than Nvidia’s, with revenue forecasted to increase by 16.6% in 2024 to $26.4 billion, while earnings are forecasted to grow by 41%. Additionally, AMD’s AI-focused business is not expected to take off like Nvidia’s, with projected revenue from this market paling in comparison to Nvidia’s.

The Verdict

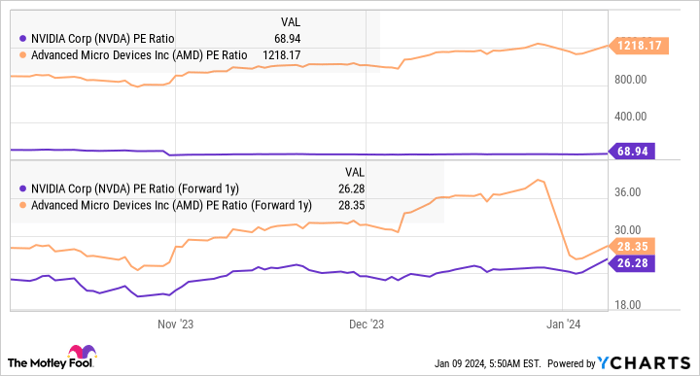

It is evident that Nvidia is poised to achieve faster growth. What further solidifies Nvidia’s position over AMD is the valuation. Nvidia appears significantly cheaper than AMD in terms of forward and trailing earnings multiples, making it an attractive bet for investors seeking semiconductor stocks.

Investor’s Beware: Nvidia Continues to Rise While Competitors Falter

As the semiconductor market continues to surge and hot trends such as AI gain momentum, investors seek optimal avenues for capturing this growth. Recent data demonstrates that Nvidia outshines its competitors, particularly Advanced Micro Devices (AMD), making it an attractive prospect for investors.

Nvidia vs. AMD: A Profitable Choice

Investors keen on capitalizing on the semiconductor market’s expansion this year are better off betting on Nvidia over AMD. Aside from the sizzling tech trends such as AI, PE ratio data indicates Nvidia as a prime pick for those pursuing profitability in the current market climate. This trend fosters a contrasting outcome for its competitors, including AMD.

The Motley Fool’s Take on Nvidia

The Motley Fool recently disclosed a list of top stocks for investors to consider, with Nvidia not making the cut. While this revelation may dampen spirits, seasoned investors understand that market movements can often defy traditional perceptions. Maintaining a diversified approach to investment is the fundamental guiding principle for many, a stance that often prompts skepticism when certain stocks, such as Nvidia, are overlooked.

The renowned Stock Advisor service, a respected voice within the investor community, vouches for an intuitive, success-driven blueprint that promises fruitful guidance on constructing a robust portfolio. The service has fiercely outperformed the S&P 500 since 2002, affirming its status as a stalwart ally to investors exploring the nuances of the financial market. The appeal of such tried-and-true advisories continues to resonate with a broad spectrum of investors, reflecting an enduring preference for clarity and strategic foresight.

“Amid the mystique of financial forecasts, embracing a multidimensional approach is akin to crafting a sturdy life raft in a tempestuous sea.”

Summary

As the topography of the market undulates, the choice to invest in Nvidia presents a compelling proposition for astute investors. Notably, Nvidia’s trajectory, eclipsing that of its competitors, accentuates the company’s promising stand in the semiconductor domain.

The Motley Fool’s investment insights furnish a holistic perspective on market movements. Hence, investors who proactively traction this guidance may discern a wealth of opportunities, encapsulating the sheer dynamism of contemporary investment strategies. Such a narrative places Nvidia front and center in the competitive financial arena, undergirded by palpable indicators reaffirming the resilience of the company.