Every quarter, investment firms that manage more than $100 million file a form 13F with the Securities and Exchange Commission (SEC). I find the 13F to be a valuable tool because it breaks down in detail which stocks institutional investors are buying and selling, and it can be interesting to try and identify patterns among Wall Street’s biggest money managers.

One investor that I enjoy following is Jeff Yass, the co-founder of Susquehanna International Group (SIG). During the second quarter, SIG purchased roughly 5 million shares of artificial intelligence (AI) stock Super Micro Computer (NASDAQ: SMCI) — increasing its position in the company (also known as Supermicro) by 148%.

Below, I’m going to break down the mechanics of Supermicro’s place in the AI realm and address some important topics that should be considered when investing in the company.

1. Understanding the financials of IT infrastructure

Supermicro often comes up when semiconductor companies such as Nvidia or Advanced Micro Devices are mentioned. For this reason, many investors perceive Supermicro as another chip stock — but in reality, this isn’t exactly right.

Supermicro is an IT infrastructure business that specializes in designing storage architecture for Nvidia’s and AMD’s graphics processing units (GPU). So, while demand in the chip industry has direct influences on Supermicro’s operation, the company itself is not a true semiconductor stock.

Although Supermicro has undoubtedly benefited from AI tailwinds, the financial profile below paints a pretty sobering reality.

SMCI Revenue (Quarterly) data by YCharts

Namely, Supermicro’s gross profit margin is trending in the wrong direction. Despite consistent acceleration across the top line, Supermicro’s unit economics are pretty backward.

While management has said that these headwinds will be short-lived, the reality is that IT infrastructure is not a high-margin industry. This dynamic leads me to my next important topic: competition and the risk of commoditization.

2. The competitive landscape is tough

While Supermicro has done a respectable job of fostering relationships with some of the world’s leading GPU producers, these relationships are by no means exclusive.

Supermicro competes with plenty of other businesses that offer IT architecture solutions, including Dell Technologies, Hewlett Packard Enterprise, Lenovo, and Cisco. These companies are much larger and more diverse than Supermicro, making them formidable rivals.

Broadly speaking, when the same solution is offered by many players within the same industry, companies become forced to compete on price. So, even though Supermicro’s management has been forecasting increasing operating profit, I question how profitable the company will ever become as competition heats up.

Image source: Getty Images.

3. Be aware of the shorts

I think the biggest topic investors need to be aware of when considering an investment in Supermicro is allegations made against the company by Hindenburg Research. Hindenburg is a short-seller, which means the firm has a financial interest in seeing a stock price decline.

Since Hindenburg published its short report on Aug. 27, shares of Supermicro had dropped by 16%.

To summarize, Hindenburg alleges that Supermicro’s financial controls and accounting practices may contain errors, perhaps intentionally. Considering Supermicro did wind up delaying its annual report, it’s clear why some investors sold the stock and moved on. Almost as concerning is a Wall Street Journal report that the U.S. Department of Justice is looking to Hindenburg’s claims.

With all of this said, nothing material has come from Hindenburg’s allegations yet, and it seems that the pronounced sell-off is rooted more in fear than anything concrete.

The bottom line

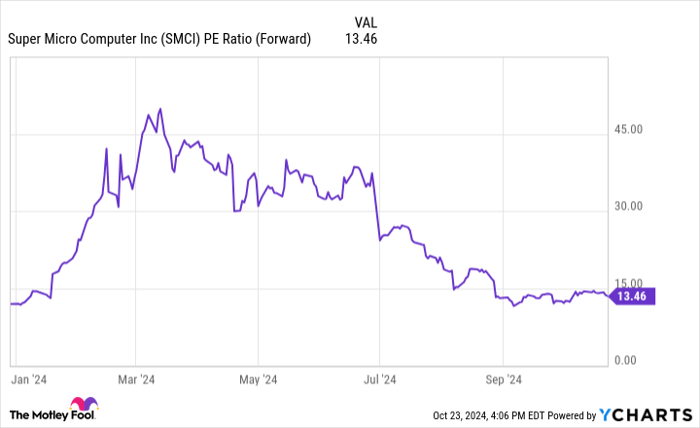

Supermicro currently trades at a forward price-to-earnings (P/E) multiple of about 13.5. As the chart below indicates, Supermicro’s valuation multiples have deteriorated in recent months as speculation rises over the company’s future.

SMCI PE Ratio (Forward) data by YCharts

I can see how the allegations against the company may spur some panic selling. Meanwhile, the packed competitive landscape does make Supermicro’s long-run profitability picture hard to forecast. Nevertheless, I see Supermicro remaining as an important business in the world of IT infrastructure.

In the near term, I think Supermicro’s most obvious catalyst is the planned launch of Nvidia’s Blackwell GPU architecture. Furthermore, as businesses continue pouring billions of dollars into AI infrastructure, such as data centers, network connectivity solutions, and GPUs, I’m hard-pressed to buy into the narrative that Supermicro isn’t well positioned for the long run.

While I understand the risks surrounding Supermicro, I see the decline in the company’s valuation as a rare opportunity to scoop up shares of a growth stock at a more reasonable price.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $867,372!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 21, 2024

Adam Spatacco has positions in Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Cisco Systems, and Nvidia. The Motley Fool has a disclosure policy.