Meta Platforms META reported third-quarter 2024 earnings of $6.03 per share, beating the Zacks Consensus Estimate by 16.18%. The figure surged 37.4% year over year.

META’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 11.34%.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Revenues of $40.589 billion beat the Zacks Consensus Estimate by 0.95% and increased 18.9% year over year. At constant currency (cc), revenues soared 23% year over year.

Following third-quarter earnings, META shares fell more than 3% in after-hours trading. Meta Platforms’ shares have gained 67.2% year to date (YTD), outperforming the Zacks Computer & Technology sector’s return of 27.6%.

Meta Platforms, Inc. Price, Consensus and EPS Surprise

Meta Platforms, Inc. price-consensus-eps-surprise-chart | Meta Platforms, Inc. Quote

Meta Platforms shares have also outperformed most of its “Magnificent 7” peers, including Apple AAPL, Alphabet GOOGL, Amazon AMZN, Microsoft, and Tesla. NVIDIA is the only Magnificent 7 stock that has outperformed META shares over the same timeframe.

Apple, Alphabet, Amazon, Microsoft, and Tesla shares have returned 19.5%, 24.9%, 26.9%, 15.1% and 3.7%, respectively. NVIDIA shares have appreciated 181.4% YTD.

META’s YTD Performance

Image Source: Zacks Investment Research

We believe Meta Platforms’ focus on leveraging AI to improve user engagement will drive top-line growth. This, along with the strong third-quarter earnings beat, is expected to help Meta Platforms’ shares surge higher in the near term.

Before diving into META’s investment prospects, let’s take a glance at its quarterly numbers.

META’s Top-Line Growth Rides on Facebook & Instagram

Geographically, revenues from the United States & Canada, Asia-Pacific, Europe and the Rest of the World (RoW) surged 15.9%, 18.6%, 22.1% and 23.9% on a year-over-year basis, respectively.

Revenues from Family of Apps (99.3% of total revenues), which includes Facebook, Instagram, Messenger, WhatsApp and other services, increased 18.8% year over year to $40.32 billion.

Family Daily Active People or DAP, defined as a registered and logged-in user who visited at least one of the Family products (Facebook, Instagram, Messenger and/or WhatsApp) on a given day, was 3.29 billion, up 4.8% year over year.

The launch of a unified video player and improved AI-powered recommendation has increased time spent on Facebook by 10%. Instagram reels continue to gain adoption, with more than 60% of recommendations coming from original posts in the United States in the reported quarter.

Generative AI Aids META’s Advertising Revenues

Advertising revenues (98.9% of Family of Apps revenues) increased 18.6% year over year to $39.89 billion and accounted for 98.3% of third-quarter revenues. At cc, revenues increased 23% year over year.

Advertising revenues from the United States & Canada, Asia-Pacific, Europe and the RoW surged 16.3%, 17.9%, 21.2% and 23% on a year-over-year basis, respectively.

Ad impressions delivered across Family of Apps increased 7% year over year, and the average price per ad jumped 11% in the reported quarter. Impression growth from Asia-Pacific, the RoW, the United States & Canada and Europe was 9%, 5%, 7% and 5%, respectively.

Meta Platforms’ saw higher retention rates among advertisers using generative AI-powered image expansion, background generation and text generation tools.

Family of Apps’ other revenues soared 48.1% year over year to $434 million, primarily driven by higher business messaging revenue growth from META’s WhatsApp Business platform.

Reality Labs’ revenues (0.7% of total revenues) increased 28.6% year over year to $270 million, driven by higher hardware sales.

META Expands Operating Margin Despite Higher Costs

In the third quarter of 2024, total costs and expenses increased 13.9% year over year to $23.24 billion. As a percentage of revenues, total costs and expenses were 57.3%, significantly down from 59.7% in the year-ago quarter.

In the reported quarter, Family of Apps expenses were $18.5 billion, accounting for 80% of Meta Platforms’ overall expenses. FoA expenses were up 13% year over year, primarily due to higher infrastructure and headcount-related costs.

Reality Labs’ expenses were $4.8 billion, up 21% year over year.

As a percentage of revenues, marketing & sales expenses decreased 150 basis points (bps), while general & administrative expenses also fell at the same rate on a year-over-year basis.

Research & development expenses, as a percentage of revenues, were 27.5%, up 50 bps on a year-over-year basis.

Meta Platforms’ employee base was 72,404 at the end of the third quarter, up 9% year over year.

Operating income of $17.35 billion jumped 26.2% year over year. The operating margin was 42.7%, expanding significantly from 40.3% in the year-ago quarter.

Family of Apps’ operating income surged 24.5% year over year to $21.78 billion. Reality Labs reported a loss of $4.43 billion compared with the year-ago quarter’s loss of $3.74 billion.

META’s Balance Sheet & Cash Flow Remains Strong

As of Sept. 30, 2024, cash & cash equivalents and marketable securities were $70.90 billion compared with $58.08 billion as of June 30, 2024.

Long-term debt was $28.82 billion as of Sept. 30, 2024, compared with $18.39 billion as of June 30, 2024.

Capital expenditures were $9.2 billion in the third quarter compared with $19.37 billion in the previous quarter. Free cash flow was $15.52 billion compared with $10.9 billion reported in the previous quarter.

The company repurchased $8.86 billion of its Class A common stock in the reported quarter and paid a dividend worth $1.26 billion.

META Offers Positive Guidance

Meta Platforms expects total revenues between $45 billion and $48 billion for the fourth quarter of 2024, assuming a neutral forex impact on year-over-year revenue growth.

For 2024, the company still anticipates total expenses between $96 billion and $98 billion. It continues to expect Reality Labs’ operating losses to increase meaningfully year over year.

META expects 2024 capital expenditure in the range of $38-$40 billion, higher than previous guidance of $37-$40 million.

Here’s Why META Shares Are a Buy Post Q3

META’s use of AI bodes well for its near-term and long-term prospects. META’s growing footprint among young adults, driven by improving recommendations, boosts its competitive prowess. AI usage is making it a popular name among advertisers. This is expected to drive top-line growth.

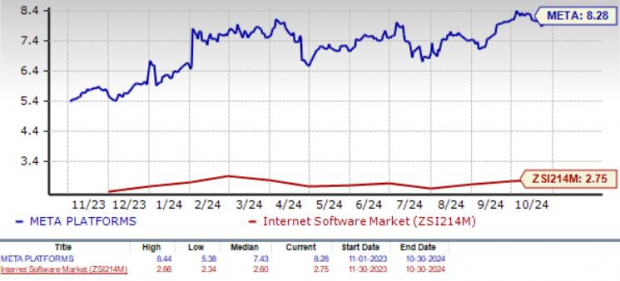

Meta Platforms shares are trading at a premium as suggested by a Value Score of C. In terms of the forward 12-month Price/Sales ratio, META is trading at 8.28X, higher than the Zacks Internet Software industry’s 2.75X.

Price/Sales Ratio (F12M)

Image Source: Zacks Investment Research

We believe Meta Platforms’ robust service offerings make the stock too attractive to ignore.

Currently, Meta Platforms carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Meta Platforms, Inc. (META) : Free Stock Analysis Report