Lucid Group, the electric vehicle (EV) maker, achieved a significant milestone by setting a new record for vehicle deliveries in the third quarter of 2024. With 2,781 vehicles delivered in the September quarter alone, this marks the third consecutive quarter of record-breaking deliveries for Lucid, bringing the total count so far this year to an impressive 7,142 units. The surge in deliveries can be largely attributed to generous discounts offered by Lucid, including up to $17,500 in savings on select models. This pricing strategy has not only made Lucid vehicles more affordable but has also driven up demand substantially.

One of the key highlights for Lucid is its upcoming electric SUV, Gravity, slated for launch later this year. This move is part of Lucid’s strategy to diversify its product lineup and tap into the growing EV market effectively. As the company gears up for its next phase of growth, it poses an interesting question for investors – is the current price of the stock, still under $5, a compelling buy? Analyzing Lucid’s performance, growth prospects, and potential challenges will shed light on this dilemma.

Lucid’s Strategic Advantages

Lucid’s trajectory is promising, with deliveries showing a consistent growth pattern. In addition to its luxury Air sedan, Lucid has ambitious plans to introduce new models, including the upcoming Gravity SUV. This SUV will feature Tesla’s NACS charging connector and access to a vast network of Superchargers, providing convenience for Lucid owners. Looking ahead, Lucid aims to roll out a mid-size electric crossover by 2026, priced competitively under $50,000 to challenge Tesla’s Model Y. This move, coupled with Lucid’s cutting-edge powertrain technology, the Atlas unit, is expected to give the company a significant competitive edge in the market.

Another feather in Lucid’s cap is its strong financial backing from the Saudi Arabia Public Investment Fund (PIF), its largest shareholder. With over 60% ownership, PIF has been a crucial source of funding for Lucid, supporting its operations and investment in new EV offerings. Lucid ended the second quarter of 2024 with $4.3 billion in liquidity and secured an additional $1.5 billion in funding from a PIF affiliate in August 2024. This financial cushion is anticipated to sustain Lucid’s operations well into the fourth quarter of 2025.

Looking at the financial projections, the Zacks Consensus Estimate for Lucid’s 2024 revenues stands at around $760 million, reflecting a healthy 28% year-over-year growth. Moreover, the estimated loss per share is narrower at $1.27, compared to $1.36 in the prior year, indicating a positive trend in the company’s financial performance.

Challenges on the Horizon for LCID

Despite Lucid’s impressive delivery figures, the company is facing production challenges. In the third quarter, Lucid’s production stood at 1,805 vehicles, showing a decline of over 14% from the previous quarter. To reach its 2024 production target of 9,000 vehicles, Lucid will need to significantly enhance its production capacity in the final quarter of the year. Notably, its competitor Rivian recently revised its production forecast downward due to supply chain constraints, emphasizing the industry-wide challenges faced by EV manufacturers.

A critical concern for Lucid is its reliance on incentives to drive deliveries. While discounts have boosted sales, they have also exerted pressure on Lucid’s margins. With hefty price cuts of up to $17,500, Lucid is grappling with maintaining its luxury brand perception in the market. The aggressive pricing moves suggest that Lucid may be struggling to compete effectively with Tesla and risks eroding its brand positioning in the EV sector.

Moreover, Lucid’s cash burn remains a troubling issue, compounded by its significant dependence on external funding. Despite a reduced negative free cash flow of $741.3 million in Q2 2024, compared to the previous year, the cash burn rate is concerning. While the support from PIF has kept Lucid afloat, questions loom over its long-term sustainability. The company must demonstrate its ability to scale production efficiently and achieve profitability amidst intensifying competition in the EV market.

Price Performance and Valuation of LCID Stock

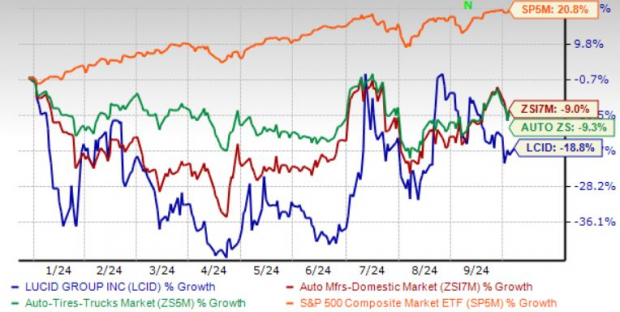

Following its public debut in 2021, Lucid’s stock has failed to live up to its delivery targets, leading to a steep decline in stock value over three years. The stock has plummeted nearly 85% during this period and has dropped 20% year-to-date, underperforming industry benchmarks and the S&P 500 index.

Year-to-Date Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, Lucid appears relatively expensive with a price-to-sales (P/S) ratio of 6.34, compared to Rivian’s P/S ratio of 1.89. Despite its low stock price, Lucid’s valuation metrics suggest a high level of risk, making it a potentially precarious investment for value-oriented buyers. The stock carries a Value Score of F, indicating cautious optimism among investors.

Image Source: Zacks Investment Research

The Verdict

While Lucid has made significant strides in 2024, surpassing delivery records and expanding its product portfolio, caution is warranted for potential investors. The company’s heavy reliance on external funding, persistent cash burn, and ongoing production bottlenecks raise red flags about its long-term viability. Despite the promise of new models like the Gravity SUV and mid-sized crossover, Lucid must address its operational challenges to sustain growth.

Investors seeking a high-risk, high-reward opportunity may find Lucid intriguing; however, those prioritizing stability may opt to observe from the sidelines for now. With a Zacks Rank #3 (Hold) assigned to LCID, cautious optimism surrounds the stock at present.