A little over a year ago, the markets began their climb out of the bearish abyss. Growth stocks surged, leading investors to ponder when a definitive bull market would take hold. That time is now upon us, marking a promising start to 2024. The S&P 500 recently reached a new peak, cementing the market’s optimistic phase of expansion and growth.

Adding to the fervor, historical data indicate that bull markets typically endure longer than their bearish counterparts, providing ample time for investors to reap the benefits. To maximize the potential of this bull market, investing in growth stocks is a wise move. They have a propensity to thrive in robust market conditions and periods of economic resurgence. Here are the top growth stocks to consider acquiring in 2024.

Image source: Getty Images.

Amazon: Navigating Growth Waters

Amazon (NASDAQ: AMZN) remains a prime growth stock due to its dominance in two flourishing markets: e-commerce and cloud computing. The company is actively investing in the burgeoning field of artificial intelligence (AI), bolstering its earnings trajectory in multiple ways.

AI is enhancing efficiency across Amazon’s operations, leading to cost reductions. Additionally, Amazon’s cloud computing arm, Amazon Web Services (AWS), furnishes AI tools to clients. Given the soaring demand in this domain, AWS’ AI offerings could fortify client retention, amplifying AWS’ revenue. This holds substantial importance as AWS has historically been a profit driver for Amazon.

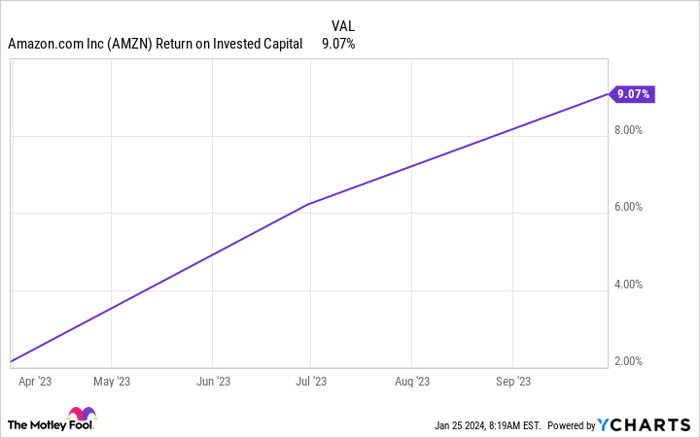

Amazon’s recent initiatives to revamp its cost structure amid mounting inflation and other challenges have yielded positive results. Despite reporting its first annual loss in nearly a decade in 2022, Amazon swiftly transitioned to quarterly net income gains and a shift from cash outflow to inflow early last year. In the latest quarter, the company’s net income surged threefold, with free cash flow surging to over $21 billion. Return on invested capital has also been ascending over the past year.

AMZN Return on Invested Capital data by YCharts

These strategic maneuvers are poised to benefit Amazon in prosperous times. Notably, the company has augmented efficiency across its fulfillment network, transitioning to a regional model from a national one in the U.S. The ensuing reduction in delivery distances is driving enhancements in Amazon’s “cost to serve,” with significant potential for ongoing advancements.

Consequently, despite Amazon’s stock ascent last year, its growth potential is far from exhausted, positioning it as a standout player in this bull market.

Carnival: Riding the Waves of Recovery

Carnival (NYSE: CCL) weathered a challenging period during the pandemic’s onset, with halted sailings precipitating a tumultuous phase for the world’s largest cruise operator. However, the company has since rebounded swiftly, with surging demand for cruise getaways evident in Carnival’s robust revenue and bookings. In the latest quarter – the fiscal fourth quarter – Carnival reported record revenue, with bookings around Black Friday hitting an all-time high for that period.

For the fiscal year concluding in November, Carnival achieved record-breaking revenue exceeding $21 billion and commenced the new year with its most favorable booked position ever, encompassing occupancy and pricing considerations. This resurgence facilitated earning upswings, exemplified by Carnival reporting a lower-than-expected U.S. GAAP net loss of $74 million for the year and positive adjusted net income of $1 million.

Carnival’s debt burden has been a principal concern for investors. While the company accumulated significant debt during the initial pandemic phase due to suspended cruises, Carnival has made substantial headway in debt reduction, slashing debt by $4.6 billion from its peak. Continued growth in adjusted free cash flow, as projected by Carnival, is expected to contribute to further debt repayment.

Record booking volumes and customer deposits at Carnival bear witness to optimistic revenue prospects. The company’s initiatives to streamline operations and curtail fuel expenses amplify its earning potential. Given Carnival’s steadfast progress in its recovery and growth narrative, now presents an opportune time to consider investing in this stock.

Apple: Orchestrating Prolific Growth

Apple (NASDAQ: AAPL) is a colossal presence in the market, courtesy of its flagship products like the iPhone and Mac computers. Nevertheless, this market dominance does not signify a growth plateau for the company. In fact, three key drivers are poised to propel Apple’s earnings growth well into the future.

Image source: Getty Images.

Foremost among these is Apple’s robust brand loyalty, perpetuating customer allegiance towards purchasing the latest iPhone or Apple Watch instead of experimenting with rival offerings. This brand loyalty forms a crucial part of Apple’s moat, namely its competitive advantage – an essential attribute that could sustain Apple’s ascendancy over the long haul.

Apple’s Services Business Driving Record Revenue

Record Revenue from Services

Apple’s growth driver is its services business, which reported record revenue in the latest quarter. This surge in revenue can be attributed to the loyalty of Apple’s customer base, who subscribe to various services through their devices, including digital content and cloud storage. The company’s formidable user base, with an installed base of active devices topping 2 billion, has now become a consistent source of recurrent revenue.

Profitability of Services Business

Notably, Apple’s services business also boasts higher gross margins compared to its products. In the most recent quarter, the gross margin on services was 70%, in contrast to the 36% gross margin on products.

Continuous Expansion of Customer Base

Apple continues to attract new customers, indicating that the company has not yet reached its peak in terms of gaining market share. In the latest quarter, half of Mac and iPad buyers were new to those products.

Promising Growth Story

Considering these factors, Apple’s growth trajectory appears to be enduring, and the new bull market could mark an exhilarating chapter for both the company and its shareholders.