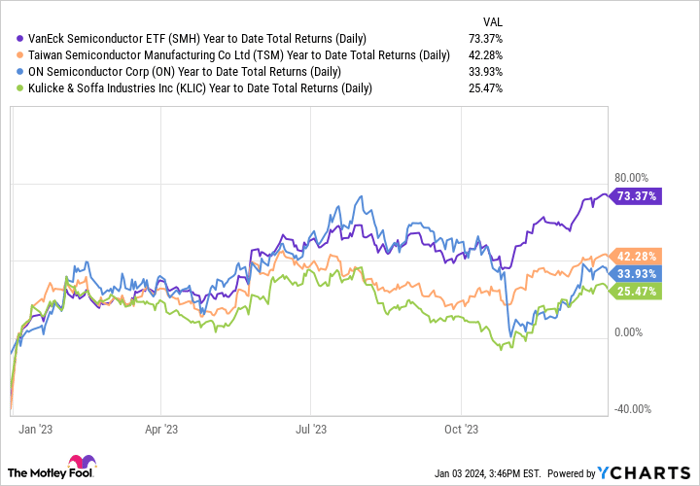

To say that 2023 was a good year for semiconductor stocks is an understatement. The sector, at least as defined by the VanEck Semiconductor ETF (NASDAQ: SMH), rocketed 73.4% in 2023! So if you had shied away from this volatile yet important part of the market, you likely missed out on some of the biggest gains of the year.

The artificial intelligence (AI) revolution no doubt played a big part, causing some of the largest names like Nvidia and Advanced Micro Devices to rise 239% and 128%, respectively.

A Closer Look at the Opportunities

But there are other, really important chip companies with strong business models and important long-term growth trends that lagged the sector. On that note, the following three stocks still look like bargain-priced options in the red-hot sector today.

SMH Year to Date Total Returns (Daily) data by YCharts.

Opportunity 1: Taiwan Semiconductor Manufacturing

The world’s largest chip foundry Taiwan Semiconductor Manufacturing (NYSE: TSM) was up “only” 42.3% in 2023, including its 1.9% dividend. But that left the stock only trading around 18 times trailing earnings and under 16 times this year’s earnings estimates.

That’s certainly a more-than-reasonable price to pay for the world’s largest foundry that makes basically all of the world’s most important chips, from Nvidia’s H100 accelerators to AMD’s Instinct MI300 to Apple‘s M-series laptop and A-series mobile processors.

2023 was a down year for many key semiconductor markets, including both PCs and smartphones, which are still the largest chip end markets today. Investors became disappointed in TSMC’s results mid-year after second-quarter earnings when management revealed that AI chips made by Nvidia only made up a mid-single-digit percentage of the overall industry. Given how huge Nvidia’s growth was last year, that appeared to surprise some investors, who may have been hoping for a bigger AI surge for TSMC.

But TSMC stock clawed its way back toward the end of the year when growth surprised to the upside. In its Q2 earnings call with analysts, TSMC management revised down prior guidance for the year, anticipating revenue would fall around 10% for the year.

However, things turned out much better than anticipated, as AI demand remained very strong while other key markets started to turn around. TSMC releases its monthly revenue, and through November, its 11-month revenue was only 4.1% below that of 2022 — much better than the anticipated 10% decline.

Eventually, all of those laptops and smartphones bought during the 2020 to 2021 pandemic period will have to be replaced, likely by higher-end chips for AI PCs and other advanced machines. Furthermore, AMD’s CEO Lisa Su just increased her outlook for the AI chip market to $400 billion by 2027, up from her June prediction of just $150 billion.

While TSMC said it expects AI chips to grow from a mid-single-digit percentage of its revenue to a mid-teens percentage over time, that is probably conservative. With a larger AI market growing very fast as other markets are turning around, look for TSMC to post strong growth in the year ahead.

Opportunity 2: On Semiconductor

The electric vehicle (EV) market is projected for long-term growth, especially as technology improves and costs come down. But 2023 saw a slowdown in the market, causing many EV-related stocks to plunge in Q2 and Q3, like silicon carbide leader On Semiconductor (NASDAQ: ON).

This year, the supply chain shortages that plagued the industry in 2021 and 2022 were alleviated, leading to ample supply. Moreover, the company is set to improve margins as it brings its new 300mm East Fishkill plant up to speed, so there is also a self-help, margin-improvement story here as well.

Image source: Getty Images.

Opportunity 3: Kulicke and Soffa

The AI revolution has put a big focus on whichever chipmaker can produce the fastest and most power-efficient chip at the most advanced node. But investors shouldn’t ignore chip-packaging companies either, such as industry leader Kulicke and Soffa (NASDAQ: KLIC). These types of companies are somewhat less sexy and use more commoditized machines that connect chips together on a motherboard or even to each other, usually through copper wires or small copper “bumps.”

But as chips become more complex, a greater focus will come on packaging. This is especially true as power and electricity concerns come to the fore, since more powerful chips require more electricity and generate more heat. AI chipmakers are even beginning to construct chips made of “chiplets,” which are optimized pieces.

The Rise of “Superchips” and What it Means for the Kulicke and Soffa Stock

Individual computer chips are fast becoming the building blocks of the digital age. A look at the recent developments in the semiconductor industry reveals a trend towards integrating smaller units of silicon into “superchips.” These superchips are formed by stitching together multiple chiplets using advanced packaging technologies, creating a powerful unit. For example, AMD’s MI300 is composed of 13 different chiplets.

Market Position and Revenue Segments

Kulicke and Soffa, a major player in the semiconductor packaging equipment sector, has a dominant position in “legacy” ball bonder packaging equipment. However, the demand for this equipment tends to fluctuate with industry cycles. The company also has smaller revenue segments in emerging technologies, such as thermocompression bonding for chiplets, EV battery packaging, and microLEDs – a cutting-edge screen technology which is currently prevalent in high-end electronics and could potentially expand to smartphones in the future.

Financial Performance

Similar to TSMC, Kulicke’s primary business of ball bonding has experienced a downturn, leading to a significant decline in earnings over the past year. From $7.09 in 2022, the company’s earnings plummeted to only $0.99 in 2023. However, when considering the extremes, the company’s average earnings power is estimated to be around $4 per share. At a stock price of just $51.50, with approximately $13.40 in cash on the balance sheet and no debt, the company’s enterprise value (roughly $38 per share) in relation to average earnings ($4) would be less than 10.

Investment Perspective

Irrespective of the analytical angle, it’s evident that Kulicke and Soffa’s stock is attractively priced. From any vantage point, the stock appears to be a cost-effective option for potential investors, making it an under-the-radar pick in 2024.