Apparel juggernauts like Lululemon and Nike are weathering the storm of economic uncertainties, each facing an approximate 8% drop in stock value over the past year. Nonetheless, Lululemon stands resilient, assuring investors of its continued growth potential as it outpaced first-quarter revenue and profit projections, with Nike slated to unveil its quarterly report later this month.

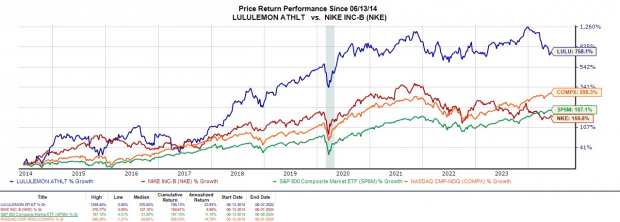

With LULU shares plunging 37% year-to-date, shareholders may find themselves pondering whether now is the opportune moment to delve into stocks of the trendy yoga-themed athletic wear champion, anticipating a recovery amidst its illustrious record.

Image Source: Zacks Investment Research

Assessment of Q1 Performance & Revenue Projections

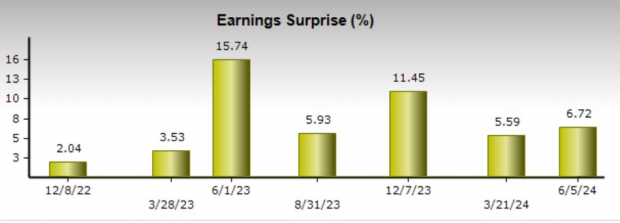

Underscoring its unwavering brand loyalty, Lululemon’s Q1 revenue of $2.2 billion surged by 10% from the corresponding quarter, just slightly surpassing the estimated $2.19 billion. Moreover, its earnings per share (EPS) for Q1 at $2.54 exceeded expectations by 7% and exhibited an 11% hike from a year earlier. Noteworthy is the fact that Lululemon has now beaten earnings projections for 16 consecutive quarters since September 2020.

Image Source: Zacks Investment Research

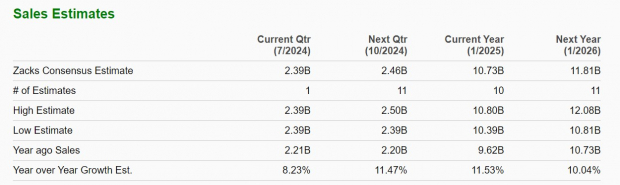

Anticipating the second quarter, Lululemon forecasts a revenue growth rate of 9%-10%, slightly surpassing the current Zacks Consensus of 8.23%, or $2.39 billion in sales (Current Qtr below). The company maintains its full-year revenue growth expectations in the 10%-11% range, with projections calling for 11.53% growth (Current Year).

Image Source: Zacks Investment Research

Future Outlook on Earnings per Share (EPS)

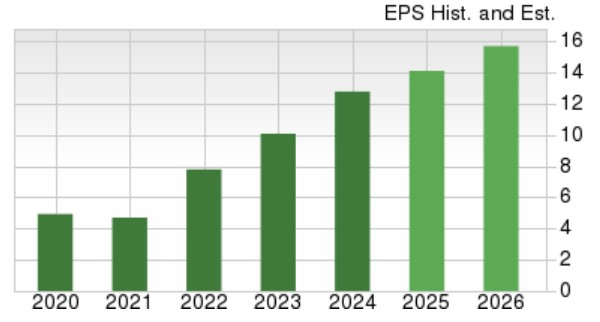

According to Zacks estimates, Lululemon’s annual earnings are expected to climb by 11% in the current fiscal year 2025 to $14.14 per share, compared to $12.77 in FY24. Furthermore, the forecast for FY26 EPS indicates an additional 11% surge to $15.68.

Image Source: Zacks Investment Research

Key Takeaways

Despite looming apprehensions regarding consumer spending slowdowns, particularly concerning upscale apparel items, Lululemon’s stock maintains a Zacks Rank #3 (Hold). The Q1 results from Lululemon served to reaffirm a promising earnings outlook, coupled with the enticing factor that LULU currently trades at its most affordable price-to-earnings (P/E) ratio of 22.9X since its initial public offering. Long-term investors could reap rewards at current levels, while more favorable buying opportunities may lie ahead.

Zacks Names “Single Best Pick to Double”

From a myriad of stocks, 5 Zacks experts have each identified their top choices likely to skyrocket by over 100% in the months ahead. Choosing from these five, Director of Research Sheraz Mian selects one with the most explosive potential of all.

It’s a lesser-known chemical company that has soared by 65% over the past year, yet remains remarkably affordable. With persistent demand, escalating 2022 earnings anticipations, and $1.5 billion allocated for share buybacks, retail investors may seize this opportunity at any moment.

This company could outshine or even surpass other recent Zacks’ standout performers such as Boston Beer Company, which surged by +143.0% in slightly over 9 months, and NVIDIA, which skyrocketed by +175.9% within a year.