Tesla (TSLA) is on the brink of unveiling its third-quarter 2024 financial performance post-market this Wednesday. Analysts expect earnings per share of 58 cents and revenues of $25.6 billion. A slight upward revision in earnings forecasts has transpired in recent days, although a 12.12% year-over-year decline is anticipated in the bottom line. Contrarily, the revenue estimate indicates a more favorable trajectory, displaying a 9.5% growth potential.

Throughout the current year, consensus views anticipate Tesla’s revenues to hit $98.7 billion with a modest uptick of 2%. The earnings per share projection for 2024 stands at $2.25, reflecting a significant dip of around 28% from the previous year.

Tesla’s track record in meeting EPS estimates has been gilded – with lowlights on all occasions, boasting an average negative earnings surprise of 8% through the past four quarters.

Decoding Tesla, Inc.’s Price and EPS Surprise

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Tesla’s Earnings ESP suggests a cautious tone for investors with a -1.28% figure and a Zacks Rank #2. The amalgamation of a positive Earnings ESP and a Zacks Rank #1, 2, or 3 typically indicates a higher likelihood of an earnings beat, which does not fortify Tesla’s current standing.

Sub Rosa of TSLA’s Q3 Results

During the third quarter, Tesla rolled out 469,796 vehicles, including 443,668 Model 3/Y units. Deliveries stood at 462,890 units, slightly under the Zacks Consensus Estimate. Despite the minor stumble, deliveries demonstrated a year-over-year uptick for the first time in 2024, escalating by 4.3% compared to the preceding quarter.

Automotive revenues for this quarter are forecasted at $22.2 billion, indicating a 13% surge compared to the prior year. Discount initiatives to traction demand might have amplified sales figures, albeit at the potential expense of margins. Forecasts predict a decline in Tesla’s automotive segment gross margin to 18.3% from 18.7% in the corresponding quarter last year.

Amidst squeezed margins in automotive activities, Tesla’s energy generation and storage sector is garnering momentum. Buoyed by robust demand for Megapack and Powerwall products, this segment anticipates revenue growth of 39%, with gross profit poised for a robust 45% expansion.

Meanwhile, Tesla’s Services/Other segment eyes a revenue uptick to $2.3 billion, underpinned by a burgeoning supercharging network. Leading automobile manufacturers like General Motors, Ford, and Stellantis adopting Tesla’s NACS charging standard augur well for this division’s future outlook.

Tesla’s Stock Trajectory & Valuation

Year-to-date, Tesla’s stock has retreated by approximately 11%, surpassing industry and sector benchmarks but falling short of S&P 500’s growth trajectory.

Comparative YTD Stock Analysis

Image Source: Zacks Investment Research

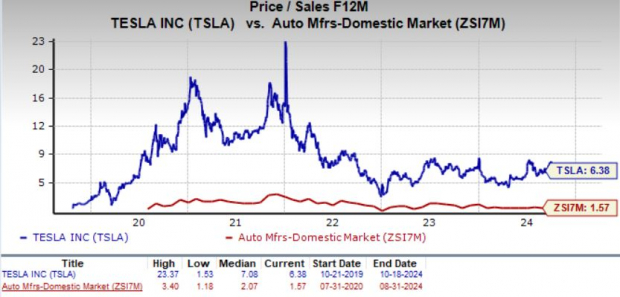

In evaluation terms, Tesla’s valuation appears slightly bloated. Boasting a forward sales multiple of 6.38, the company exceeds the industry’s 1.57 benchmark, albeit hovers beneath its five-year average.

Image Source: Zacks Investment Research

Charting Strategies Ahead of TSLA’s Pre-Q3 Earnings Call

Tesla faces the dual discord of thinning automotive margins and investor ambiguity post the Robotaxi shake-up, precipitated by a paucity of clarity on its ridesharing scheme. While uncertainties loom large, Tesla’s technological forays reveal promise. Initiatives like the Optimus humanoid project and the Full Self-Driving Beta software underscore Tesla’s commitment to innovation. The company’s expedited plans for introducing affordable EV models signal avenues for future growth. Furthermore, the lucrative Energy Generation and Storage business bolsters Tesla’s profit margins, while the expanding NACS charging network spells revenue uptrends.

As scrutiny intensifies ahead of the earnings unveiling, investor attention will pivot to Tesla’s revenue progression, margins, and cash flow vitality as barometers of its overall financial robustness.

Tesla’s recent stock adversity post the Robotaxi fiasco caught many off guard. Nonetheless, Ark Invest seized the opportunity, acquiring close to $3 million in Tesla shares – emblematic of their strategy to prospect amid dips and technical downturns. Investors leveraging Tesla’s current ebb post the underwhelming “We, Robot” event may envision a fortuitous

The Landscape of Semiconductor Stocks: Seizing Opportunity Amidst Uncertainty

The world of investing is akin to navigating choppy waters with a rickety boat – fraught with risk but brimming with promise. As investors brace for the unveiling of upcoming results in the tech sector, one beacon of hope shines bright: semiconductor stocks.

The Rising Star

In a market dominated by giants like NVIDIA, a newcomer emerges – a mere 1/9,000th of the size but poised for a meteoric rise. While NVIDIA soared over 800% following a recommendation, this top chip stock promises even greater potential for growth.

Fueled by robust earnings expansion and a burgeoning clientele, this stock is strategically positioned to satiate the insatiable hunger for Artificial Intelligence, Machine Learning, and the Internet of Things. Projections indicate that the global semiconductor industry is set to balloon from $452 billion in 2021 to a staggering $803 billion by 2028.

The allure of this semiconductor stock lies not just in its current stature but in its future trajectory – a trajectory pointing towards exponential ascension amidst the technological revolution sweeping across industries.

Unveiling Opportunities

As the investment landscape continues to evolve, seizing opportunities in semiconductor stocks offers investors a chance to ride the wave of innovation and technological advancement. While uncertainty may loom on the horizon, it is often amid such turbulence that the most rewarding investments are made.