The buzz around artificial intelligence (AI) set the markets on fire in 2023, propelling the tech-heavy Nasdaq up by an impressive 40%. At the forefront of the AI revolution stands semiconductor manufacturer Nvidia (NASDAQ: NVDA), hailed by Wall Street luminary Dan Ives of Wedbush Securities as the godfather of AI.

Despite its remarkable 237% surge in the prior year, the question remains whether Nvidia’s stock is truly undervalued. Let’s unravel why the company is leading the AI charge and contemplate if now is the opportune moment to capitalize on this sleeper stock.

The Unprecedented Demand

Nvidia has revolutionized graphics processing units (GPUs), with its A100 and H100 chips being the cornerstones of its GPU line. The H100 chips are currently witnessing an unparalleled surge in demand.

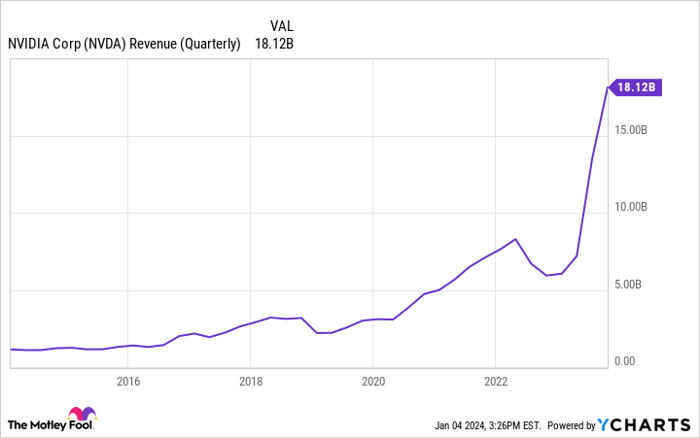

NVDA revenue (quarterly) data by YCharts.

Nvidia’s third-quarter revenue for fiscal 2024, ending Oct. 29, hit a record $18.1 billion, marking a staggering 200% year-over-year increase. Furthermore, the company’s profits soared by almost 500% in the first three quarters of its fiscal year.

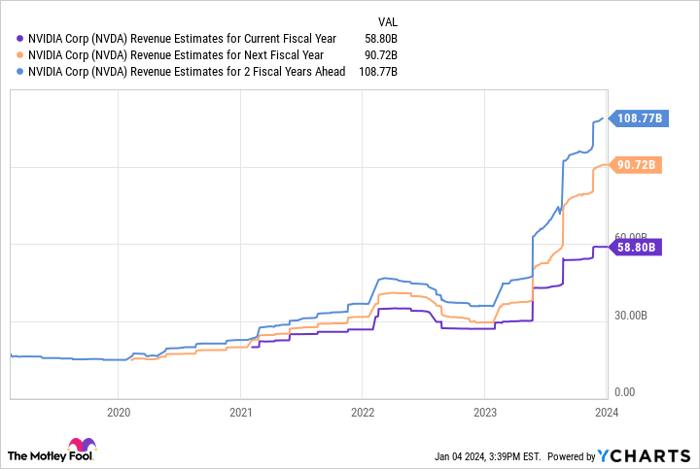

Notably, Wall Street projects a 54% surge in revenue this fiscal year, followed by a 20% increase the subsequent year. While this signifies a deceleration in revenue growth, it aligns with the natural growth trajectory of a tech giant like Nvidia, especially considering the competitive landscape of the AI application market for data center GPUs.

NVDA revenue estimates for the current fiscal year, data by YCharts.

With 2024 poised to be another milestone year for Nvidia, investors are naturally inquisitive about the stock’s attractiveness from a valuation perspective.

Valuation Under the Microscope

As of the latest data, Nvidia’s stock is trading at a forward P/E multiple of 24.8, while its top competitor, Advanced Micro Devices, commands a forward P/E of 37. This valuation dissonance against its closest rival, given Nvidia’s unassailable market share in AI data center GPUs, is perplexing.

Moreover, when juxtaposed with the forward P/E of the S&P 500, which stands at 21.7, Nvidia’s valuation appears to be a conundrum in light of its exceptional performance in 2023 and the bullish outlook for the current year.

While the stock’s ascent to the $1 trillion market-cap club and the exuberance that ensued might have created an impression of a pricey stock, a closer look at the multiples suggests that Nvidia is in fact growing into its valuation, possibly rendering it a bargain.

I am betting that Nvidia will continue benefiting from the sustained tailwinds of AI, and now seems like an auspicious moment to gradually build a long-term position in the stock at an attractive price.

Before you contemplate investing in Nvidia, ponder this: The Motley Fool Stock Advisor team has identified what they consider to be the 10 best stocks to buy now, with Nvidia not making the cut. Do you buy into this narrative or is Nvidia an uncut gem waiting to be unearthed?

*Stock Advisor returns as of December 18, 2023.