Rivian (NASDAQ: RIVN) has emerged as a strong candidate to move from young electric vehicle (EV) start-up to significant player. While the stock has trended lower as EV sales growth has slowed in the U.S., the company is still an intriguing long-term play you can scoop up on the cheap right now.

But before you dive in, make sure you understand and can answer these three questions.

Impact of Amazon’s influence on Rivian

At first glance, this question might seem odd. After all, Amazon‘s order for a total of 100,000 electric delivery vans by 2030 is a huge positive for the company, even if many investors were disappointed to learn that as of October, it had only delivered about 10,000.

However, what many investors overlook is that Amazon is also a significant holder of Rivian stock. In fact, Amazon owns a 17% stake in the young EV maker. On one hand, that’s good news because what’s good for Rivian is also good for Amazon. On the other hand, if Amazon were to decide to cash out its stake in Rivian, it would create an overhang on the stock that could last for many months.

It wouldn’t be the first time Rivian has dealt with a situation like this. Ford Motor Company had originally planned to develop a platform in partnership with Rivian, but eventually walked away and slowly sold off its stake in the EV maker. (Ford would later use the profits from that sale to dish out a special dividend to its investors.)

Rivian’s partnership with Amazon is a huge positive for the company, but be aware: If Amazon ever decides to sell its stake, that could depress Rivian’s stock price for months.

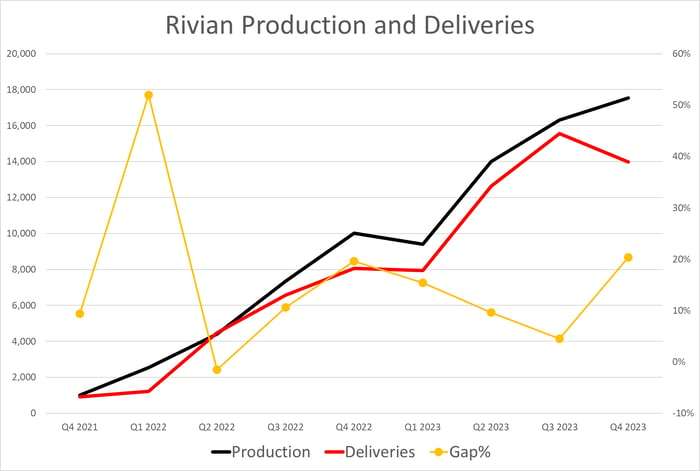

Path to Gross Profitability

One big milestone that Rivian is approaching is becoming gross profit positive. Management estimates that it’ll happen in 2024 — if and when it does, that would go a long way toward convincing investors to jump on board, and show that the company should eventually become profitable enough to fund its operations without taking on more debt or diluting shareholders through the issuance of additional shares.

To reach positive gross profit in 2024, the company will have to significantly ramp up its production and deliveries — perhaps even double them from 2023 levels. Will it be able to do those things in 2024?

Chart by author. Data source: Rivian production and delivery releases.

As you can see, there was a slight weakness in fourth-quarter deliveries that was largely blamed on Amazon not accepting large shipments of delivery vans during the peak holiday season — which is understandable.

But for the company to become gross profit positive, growth must resume in production and deliveries in the first quarter and beyond.

Rivian’s Home Run Moment

With any young company, investors are looking for a home run moment or catalyst that could spark a surge in the stock price. Rivian absolutely is closing in on one such moment: The day that its second factory opens up for commercial production in Georgia and begins rolling out the Rivian R2. Those SUVs are expected to be priced between $40,000 and $50,000, which will open the door for more mainstream consumers to consider Rivian. Investors can expect this home run moment sometime in 2026 — unless the construction and ramp-up hit speed bumps that push the timeline back.

Rivian also recently made an intriguing hire that it considers a big win: DJ Novotney, an Apple veteran (and vice president of hardware engineering) who was a notable participant in the development of the iPod, iPhone, and iPad, among other devices.

Novotney’s hiring comes at a perfect time, and as the new head of product management for products and engineering, it’s not a stretch to imagine that he will have a chance to put his fingerprints on the R2. That idea should excite investors.

Conclusion

Rivian has entered 2024 with momentum, and the company is doing many things right. If investors understand the potential risks inherent in Amazon’s large stake, can keep an eye on the company’s production and deliveries as it climbs toward gross profitability, and have the patience to wait for the catalyst of R2 vehicles hitting the market, there could be much upside to be had from Rivian stock over the long term as the trend of mass adoption of EVs slowly gains traction in the U.S. market.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Daniel Miller has positions in Ford Motor Company. The Motley Fool has positions in and recommends Amazon and Apple. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.